The Regulated Era 1938-1978

The Civil Aeronautics Act of 1938 was responsible for the creation of the Civil Aeronautics Board (CAB) and creating the regulated environment which would persist until 1978. The CAB had authority to:

- Control entry of new airlines and the start of new routes both interstate and internationally

- Control cessation of a route being operated

- Regulate all fares

- Award subsidies to airlines

- Control mergers and inter-airline agreements

Until 1958 the CAB also controlled safety issues. The CAB’s mandate was initially to enable ‘sound development’ of the industry whilst promoting adequate, economic and efficient services. Though not technically stopping new entrants, and competition, the CAB effectively did both as the barriers to entry were set so high as to be realistically unattainable. This was partly as all CAB decisions centred around individual route applications and part of the application required an airline to have proven capabilities to provide the service, which of course no new airline could ever have! Effectively all the existing airlines operating major trunk routes were grandfathered into the new system and the only real changes that an existing airline could make were by slow and painful route applications or the takeover of a failing airline (applications to merge two healthy airlines were almost always rejected). The CAB also required a new route entrant to be able to prove its new service wouldn’t harm the incumbent which severely limited the ability for competing services to exist plus in general the CAB wanted to limit the number of airline’s serving a market anyway.

In general operating an airline in the regulated market was quite easy and you had to be doing something seriously wrong to be losing money on a regular basis (still several airline’s managed this). The existing airlines were able to compete only on service and equipment, which tended to create a completely artificial view of the marketplace and would leave several of the incumbent airlines woefully ill-prepared for a deregulated market.

Below are pages dedicated to the different categories of airline that existed in the regulated environment:

Intra-State Airlines

During the deregulated era the only area of civil aviation where competition was allowed was internally within a State as the CAB only had jurisdiction over inter-state and international airline operations. Relatively few airlines attempted to enter the intra-state market on anything other than commuter operations but those that did proved to be popular, dynamic and often very profitable. Intra-State airline development centred primarily on three states California, Texas and Florida. Increasingly during the 1960s and 1970s the intra-state airlines fought successfully against the Trunk and Local service airlines with such success that they forced mergers upon the CAB (for example the Air West tri-merger could be seen to be partly the result of PSA’s success against Pacific Air Lines).

As deregulation began, after 1978, it was natural for the low-cost and flexible intra-state airlines to expand into the inter-state market and even international services. Though initially successful they were susceptible to over-expansion and absorption by the majors. Only Southwest Airlines survived into the 1990s and it has fundamentally changed the way the US market operates with its methods.

Here is a list of the primary inter-state airlines of the regulated era:

– Air California (later AirCal)

– Pacific Southwest Airlines

– Air Florida

– Southwest Airlines

Deregulation 1978-2014

The causes of deregulation are complex, however the heavy handed and blinkered mindset of the CAB was a major factor. For example over 75 non-trunk airlines had applied for trunk routes since 1950 and not one had been approved for service. A lack of competition did little to make the airline’s interested in efficiency or innovation whilst the unregulated intra-state airlines often shone a harsh light on their regulated big brothers. Additionally the economic and political background of the 1970s was one of deregulation and decreased state control. The majority of the major trunk airlines didn’t welcome deregulation and Braniff was so unsupportive as to refuse to believe it would continue even after it happenned (their landgrab expansion in preparation for reregulation was a major cause of their failure).

Regardless the deregulation that occurred from 1978 and really took off from 1980 enabled mass competition and a bevy of new startup airlines to enter the market. The result was near chaos and the end results unexpected. The 1980s represented a bloodbath as new startups began and failed regularly, a series of leveraged buyouts destabilised several of the majors (Eastern, Continental and TWA) and almost everyone who could consolidated to get critical mass, creating a merger mania. By 1992 very few of the startups were still around and the most of the airlines of the regulated era had vanished.

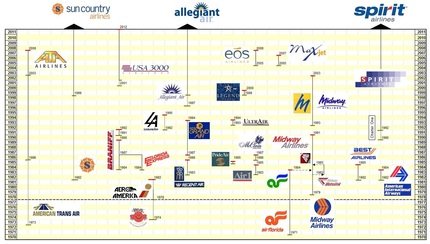

Deregulation Startups

Of all the airline’s on the below diagram only Southwest Airlines existed prior to 1978. Of the others several shone brightly for a short period (Muse Air, Northeastern) but only Midwest Express, the 2nd Frontier, Valujet/AirTran and jetBlue have shown sustained success. The majority flew only a few aircraft for a couple of years and were never profitable. Regardless they certainly added colour to the US scene.

Another method of getting involved with the deregulated scheduled market was to transition from a charter airline. This route has been taken by several airlines (American Trans Air, Sun Country, Capital, Aero America and others) but has proven to be a tough route to success. Additionally there has been a continuous stream of airlines trying to compete on service levels rather than price. This has been a disaster however it hasn’t stopped Air1, McClain, UltrAir, Legend, Regent Air, MGM Grand Air, Eos and MaxJet all trying it!

Midway Airlines was one of the first startups and survived a respectbale time however during that period it tried many routes from Chicago based startup, to buying the remains of Air Florida, business spin off (Metrolink) and Philadelphia based hub airline. Eventually its time ran out. Midway 2 had a similar tortuous life going from Raleigh Durham based hub airline to a regional player before its demise. Spirit has also changed its model however moving from a business airline to a low cost carrier has given it a chance to differentiate itself and it continues to be profitable.

Results of Deregulation

Other major features of the deregulated era have been:

- A decrease in service levels as price has become the major factor for non-business travel

- Frequent Flyer programmes and Computerised Reservation Systems

- The adoption of a hub and spoke system almost industry wide

- Commuter networks run by third tier operators in the colours of their affiliated companies feeding the hubs

- A regional jet revolution replacing most props and much mainline service

- Transition to internet based service and ticketing

- The entry of low-cost carriers (though less than outside the USA)

Rather than introduce massive competition into the market the eventual result has been the production of a handful of mega-carriers dominating the marketplace. On the flip side deregulation has enabled vastly more people to fly more cheaply than before, more efficiently without compromising safety standards. This has however come at the expenses of much turmoil and regular bankruptcies. Though the three biggest surviving airlines in 2014 are American, Delta and United the true winners of deregulation have proven to be innovative airlines like Alaska and Southwest who have survived, grown and prospered in the new landscape.